"It seems axiomatic that whenever a government fails to provide an adequate supply of currency or coin to maintain commercial trade, the people will step in to provide their own to fill the vacuum."

-- Ralph A. Mitchell and Neil Shafer [33]

The Great Depression of the 1930's was a very important chapter in history. It provided a great many important lessons for civilization, many of which are yet to be fully grasped. Much has been written about the nature and causes of the Depression, which need not be repeated here, but for those for whom the event is too remote in time to have much meaning, we will attempt a brief summary.

The Great Depression was world-wide in scope, but it was particularly severe and long-lasting in the United States [34]. It was characterized by several concurrent financial and economic symptoms, which the U. S. Department of Commerce listed as follows:

Most importantly, however, was the fact that there was little money in the hands of the people, and given their uncertainty about their prospects of getting more of it, people tended to hoard what little money they did have. Hoarding slowed the velocity of circulation, which further reduced the volume of business being transacted. Serious human needs went unmet -- until people began to organize.

Besides learning how to "make do, or do without," people began to establish mutual support structures, like workers' cooperatives, many of which would recycle and repair donated or broken items. People learned to share what they had, and to by-pass the market and financial systems. Most of these measures were considered stop-gaps to be utilized until things "got back to normal," but in some of them there seemed to be the promise of more permanent improvements. One of these "stop-gaps," which was intended to address the problem of the dearth of currency in circulation, was the issuance of "scrip."

History is full of examples of successful local initiatives aimed at providing exchange media, but the Great Depression of the 1930's saw this done on an unprecedented scale. There were literally hundreds of scrip issues that were put into circulation by a variety of agencies, including state governments, municipalities, school districts, clearing house associations, manufacturers, merchants, chambers of commerce, business associations, local relief committees, cooperatives, and even individuals. These issues went by different names, depending on who issued them and the circumstances of their issuance. Common scrip types were certificates of indebtedness, tax anticipation notes, payroll warrants, trade scrip, clearing house certificates, credit vouchers, moratorium certificates, and merchandise bonds.

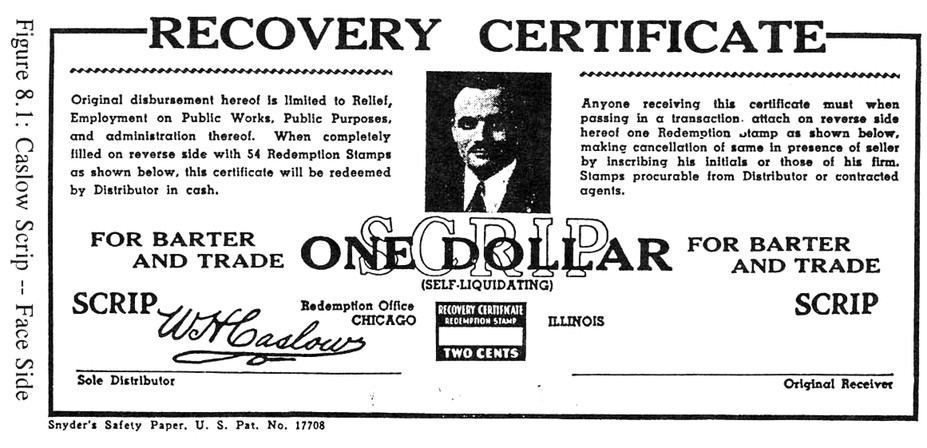

Among these scrip issues there were many failures, but there were also many impressive successes. There is much to be learned from both the failures and the successes. One interesting case was the issuance, beginning in 1933, of "Recovery Certificates" by a Chicago newspaperman named Caslow. Figures 8.1 and 8.2 show the front and reverse sides, respectively, of a Caslow Recovery Certificate.

|

|

|

As can be seen from Figure 8.2, these notes were of a variety known as "stamp scrip," and were supposed to be "self-liquidating." The inscription on the face of the notes describes the basic terms of their circulation. A 2-cent stamp was supposed to be affixed on the back and signed by the buyer each time the note was passed on in a transaction. When all the stamp spaces had been filled, a one dollar note would have changed hands 54 times and facilitated $54 worth of business. The 54 stamps which had been sold and affixed would have provided $1.08 in official money, one dollar of which would presumably be used to redeem the note, and the remaining eight cents going to cover the expense of operating the plan.

While Caslow managed to gain wide acceptance of his scrip idea, it does not seem to have worked out quite as planned. Mitchell and Shafer relate the story as follows:

"At first a small amount, it was manageable and fully accepted by a number of merchants. At one time over 500 stores were participating. Through his newspaper, "The Caslow Weekly," Caslow was able to form a large organization of self-styled "scrippers." The plan kept growing, and clubs, local clearing houses, etc., sprang up to take care of the scrip. The bulk of the scrip placed into circulation came through Caslow's using it to pay his workers. As for himself, he demanded cash for advertisements in his newspaper. As the scrip idea spread, as much as $30,000 might be issued in a single week. The plan failed, largely because there were too many field workers promoting the scrip plan and simply too much scrip. Around $1,000,000 was issued, and very little redeemed. After about two years, Caslow suspended publication of his newspaper and closed up shop." [36]

The obvious question which this story raises is, "What went wrong with Caslow scrip?" Why did a currency which enjoyed such widespread and strong support turn sour? Mitchell and Shafer do not provide enough of the details about its issuance or redemption to fully answer the question. They do, however, offer the opinion that there was "too much scrip." But was it simply a matter of too much scrip? I think this may be too simplistic an explanation. It begs the question, "too much in relation to what?"

Examination of the inscription on the face of the scrip makes several things apparent:

The eventual redemption of the scrip, therefore, seems to have depended entirely upon the integrity of Caslow and the solvency of his business. We also note that the "Original disbursement hereof is limited to Relief, Employment on Public Works, Public Purposes, and administration thereof." This is rather vague and seems to be somewhat at variance with Mitchell and Shafer's report that "the bulk of the scrip placed into circulation came through Caslow's using it to pay his workers."

The self-liquidating feature works only if the note changes hands enough times to generate sufficient stamp revenue to allow the scrip to be redeemed for cash. Far more important are the conditions under which scrip is first placed in circulation and the commitment of the original issuer himself to accept it in trade.

I think the key to the failure of Caslow's scrip might be found in his refusal to accept it in payment for his own services (advertising). One of the fundamental rules of currency issuance is that the issuer be willing to redeem his/her own currency at face value (par), and that s/he be able to generate enough value in goods and/or services to redeem the issue at the rate of about 1% per day, which is equivalent to being able to redeem the entire issue in about 3 months time. More will be said about this question later on.

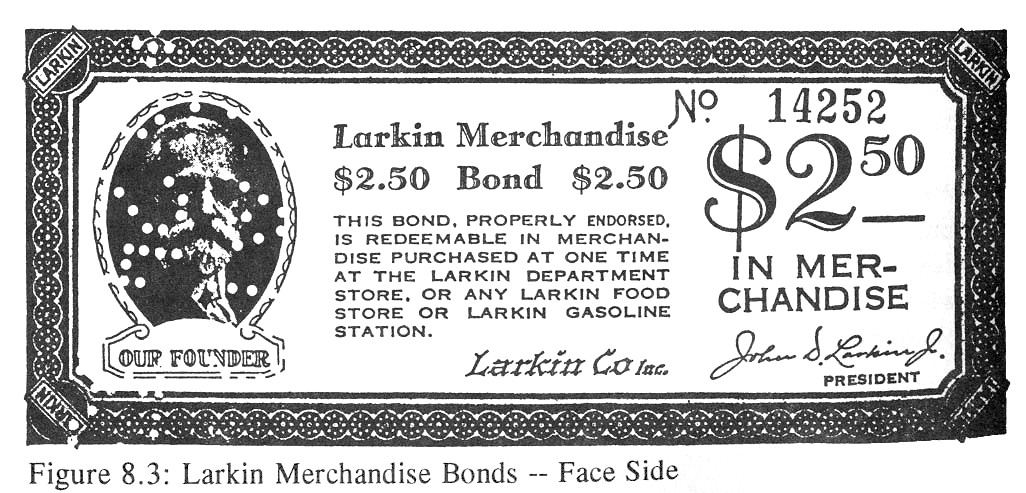

Another example, which was fairly typical of Depression scrip was one offered in 1933 by Larkin and Company of Buffalo, New York. Larkin was a large company with diverse operations including wholesale merchandising, a chain of retail stores and a chain of gasoline stations. When President Roosevelt declared his famous "bank holiday," the Larkin company issued $36,000 worth of "merchandise bonds" which it used to pay its employees.

As shown in Figures 8.3 and 8.4, these "bonds" consisted of certificates which bore the image of the company's founder and a guarantee that they would be accepted in payment for services or merchandise at any Larkin outlet in the U.S. The "bonds" were endorsed on reverse side and spent into circulation by the company. They were subsequently accepted by many Larkin customers and even other businesses. As the dearth of official currency eased, Larkin gradually retired the bonds. Company accountants estimated however, that while the bonds circulated, the original $36,000 issue had turned over enough times to allow the sale of $250,000 worth of merchandise, providing a significant boost to its business. [37]

|

Scrip was generally accepted and used to do business within a limited local area. The farther it got from home, however, the more uncertainty there was about its origin and the less confidence people would have in it. For this reason scrip tended to remain within the local economy and had the effect of stimulating local development and community self-reliance. This limited range of acceptance might seem at first to be a disadvantage of scrip, but, from the standpoint of the local economy, it is a great advantage. Toward the end of the Depression, however, as official government and central bank currencies became more widely available, scrip disappeared.

|

Some of the most notable examples of successful scrip issues were instigated by Silvio Gesell, a successful German businessman who lived much of his life in South America, and who, at one point between the first and second World Wars, served briefly in the German government. Gesell, in his once famous book, The Natural Economic Order, [38] explained his views on the nature of money and how it functions in the economy, and outlined his ideas on how it should be reformed. He originated the plan for issuing a currency known as "stamp scrip." Later, the great American economist, Irving Fisher, became a proponent of scrip and wrote a book about it. His book, entitled Stamp Scrip, described some of the subsequent scrip experiments and outlined his recommendations for proper issuance of scrip. [39] His is one of the few handbooks available on the subject.

Among the most successful and famous applications of Gesell's stamp scrip idea were the ones which took place in the small Bavarian town of Schwanenkirchen and the Austrian town of Woergl. [40] Gesell's scrip was to consist of pieces of paper of uniform size (about 8 inches by 3.5 inches) to be issued by a voluntary association of factories, merchants, a bank and any others. It would be issued in denominations of convenient amounts and be used in payment of wages and for trade. The shops who were members of the association would, of course, get all the trade. This would provide an incentive for other businesses to join, and business generally would improve.

Gesell's scrip was designed to have 52 spaces on the reverse side, one for each week of the year, and the scrip was to have the value of its stated denomination only for one week. In order for the scrip to maintain its face value, a stamp, costing two percent of the face value of the note, had to be affixed on the back, in the space allocated to that week. The stamps could be bought at the bank representing the association. This stamp device was supposed to keep the scrip from being hoarded, as people would try to spend it prior to the day the stamp had to be affixed and thus avoid the cost of the stamp. [41]

Gesell had many friends in Germany and his ideas were widely discussed but there was initially no attempt to implement them. At the time, shortly after the end of the first World War, there was currency inflation in Germany of astronomical proportions which caused severe hardships for the people. This inflation, like all inflations, was the result of improper and excessive issuance of official currency. It was part of a deliberate government policy to surreptitiously eliminate its debts by printing more money. This policy was probably a large factor in the eventual collapse of the German government, and helped set the stage for Hitler's rise to power, as he was one who exposed it.

With the coming of the Depression, the nature of the problem shifted. Money was then in short supply. Gesell's friend, Hans Timm, formed an association for the purpose of implementing the scrip idea. Timm actually had printed such stamp scrip which he called Wara, a name derived by combining two words - "Ware," the German word for goods, and "Wahrung," the German word for currency. Timm's association was called the "Wara Exchange Association." Wara became fairly well known in Germany but it was never widely used.

The village of Schwanenkirchen had a population of about 500 and its only industry was a coal mine which had been closed for two years because of the depression. The village had barely existed by means of the government dole and almost everyone was in debt. Deflation throughout Germany led to bankruptcies, suicides and overcrowded jails. The coal mine owner had heard about Wara stamp scrip and decided to try it. He got a loan of official currency (Reichsmarks) and with it bought Wara stamp scrip from the Wara Exchange Association. [42] Then, according to a report in The New Republic for August 10, 1932: [43]

"Herr Hebecker assembled his workers. He told them that he had succeeded in getting a loan of 40,000 Reichsmarks, that he wished to resume operations but that he wanted to pay wages not in Marks but in Wara. The miners agreed to the proposal when they learned that the village store would accept Wara in exchange for goods.

When, after two years of complete stagnation, the workers for the first time brought home their pay envelopes, no one was interested in hoarding a cent of it; all the money went to the stores to pay off debts or for the purchase of necessities. The shopkeepers, too, were happy. Although at first they had felt a little hesitant about Wara, they had no choice, as no one had any other kind of money. The shopkeepers then forced it on the wholesalers, the wholesalers forced it on the manufacturers, who in turn tried to pass it on to those who carried their notes, or they exchanged it at Herr Hebecker's mine for coal.

No one who received Wara wished to hold it; the workers, storekeepers, wholesalers and manufacturers all strove to get rid of it as quickly as possible, for any person who held it was obliged to pay the 2 cent stamp tax. So Wara kept circulating, a large part of it returning to the coal mine, where it provided work, profits and better conditions for the entire community. Indeed, one could not have recognized Schwanenkirchen a few months after work had resumed at the mine. The village was on a prosperity basis, workers and merchants were free from debts and a new spirit of freedom and life pervaded the town."

Continuing the account in Fisher's words: [44]

"The news of the town's prosperity in the midst of depression-ridden Germany spread quickly. From all over the country reporters came to see and write about the 'Miracle of Schwanenkirchen'. Even in the United States one read about it in the financial sections of most big papers. But no explanation was given as to the real cause of the miracle - that non-hoardable money was being tried out and that it was working marvelously."

Acceptance of Wara subsequently spread to various parts of Germany. About two thousand shops and one or two entire communities recovered by means of it. Finally, in November 1931, the German Government passed an emergency law ending the circulation of Wara. The "miracle" of Schwanenkirchen then ended and the town went back on the dole.

Another place where Wara succeeded was in the Austrian town of Woergl which, by 1932, was in dire straits. In this town of about four thousand people, many factories had closed and almost everyone in town had lost their jobs. A large amount of local taxes were unpaid. The mayor of the town had heard about Wara and decided to try it. In this case, the Wara were issued by the town, in conjunction with a number of merchants and the local savings bank. The town paid its employees half in Wara and half in official currency.

Initially, some of the local merchants refused to accept Wara, but when they saw the trade going to the other shops, they too had to climb on the bandwagon. The Wara issue was a great success. Professor Fisher describes the situation this way: [45]

"After the scrip was issued not only were current taxes paid (as well as other debts owing to the town), but many arrears of taxes were collected. During the first month alone 4,542 schillings were thus received in arrears. Accordingly, the city not only met its own obligations but, in the second half of 1932, executed new public works to the value of 100,000 schillings. Seven streets aggregating four miles were rebuilt and asphalted; twelve roads were improved; the sewer system was extended over two more streets; trees were planted and forests improved."

Unfortunately, this successful experiment was also ended under pressure exerted upon the Austrian government by the central bank. Figures 8.5 and 8.6, respectively, show the face and reverse sides of one of the Woergl notes.

|

|

To my knowledge, there is no current law which would prevent such initiatives as local scrip from being implemented today in the United States. The application of local exchange media could provide results every bit as dramatic as those obtained in Schwanenkirchen and Woergl.

Many of the scrip issues of the Depression era were defective in some way, and they should not be directly emulated, but the thing to be learned from this chapter in the history of money, is that it is possible for effective media of exchange to be issued at the local level and that the centralized control of money and finance need not limit the ability of a local economy to preserve its own health.

Some scrip issues, of course, are more credible than others. The power, productive capacity and faithfulness of the issuer are factors which affect the credibility and market acceptance of a local scrip issue. The soundness and continued acceptability of a scrip issue are dependent upon its basis of issue, the amount issued, and the means by which issuance is regulated.

Scrip issued by municipal and state governments will have a high level of credibility if it can be used to pay taxes and fees, and is accepted at par with federal money. Such scrip is said to have a "tax foundation." Scrip issued by corporations, based on their own productive capacity, will have credibility to the extent that there is a demand for their products and their current assets are sufficient to "cover" the amount of scrip issued. Scrip issued by retailers in payment for their inventories of goods will have credibility because the goods are already there in the shops waiting to be bought. This is known as the "goods foundation" or "shop foundation" of scrip. Scrip issued by individuals is theoretically possible but its acceptability will depend upon the backing provided, usually in the form of real assets.

Economic depressions are typified by a scarcity of ordinary money. Indeed, most depressions are caused by restriction of the money supply by the monetary authorities. The subsequent felt lack of adequate payment media causes people to become fearful and to hoard what money there is. This hoarding slows its rate of circulation which further reduces the volume of business being conducted. Thus, the depression deepens until money becomes plentiful again. Replenishment of the supply of official (debt) money requires not only an increased willingness of the banks to lend, but also a willingness of individuals and businesses to borrow. Their recent experience of monetary stringency during a depression, however, makes them loathe to incur new indebtedness.

The prescription for addressing this dilemma, put forth by Lord Keynes, was for government to intervene by borrowing money and spending it into circulation. It was said that the temporary deficit thus incurred could be made up later by surplus revenues once the depression was over. The experience of 60 years has made it clear that the Keynesian prescription is flawed, that "later" never comes. As we have already explained, deficits become chronic because of the very nature of the debt-money system.

The original intent of using scrip was to provide a temporary supplement to scarce official currency. But the permanent use of a locally issued and controlled exchange medium, such as scrip, has clear advantages for insulating local economies from the distorting effects of global finance and banking.

There have been numerous instances of public service companies issuing circulating notes and tokens. The familiar bus and subway tokens which are used in various places provide some idea of what might be possible. Most present-day instances of this kind intend only to provide a measure of convenience in regulating access and collecting the fares which are due.

There have been instances, however, in which tokens or notes issued by railway companies have circulated as money, being used as a means of payment, not only for railway services, but also for a wide variety of goods and services in the marketplace. According to Dr. Walter Zander, in his paper, Railway Money and Unemployment, [46] the Leipzig-Dresden Railway, sometime in the early 1800's, was authorized to issue one third of its capital in the form of "railway money certificates." These certificates, he says, remained in circulation for about forty years. Zander also indicates that during the 1920's, the German Railway issued a considerable amount of its own money.

Zander's own proposal, while apparently never implemented, was based on sound principles and makes eminent sense. My own proposals, which are outlined in later chapters, draw much of their inspiration from Zander's work and are consistent with it. While his proposal was aimed specifically at the German Railway, there is no reason why the same rationale cannot be applied in proposing that any economic entity or consortium of producers be empowered to issue circulating currency.

The official monetary system puts the cart before the horse in that money must be obtained before a purchase can be made. Whether that money be in the form of paper, coins, or bank credit, its creation is beyond the control of the producers of real wealth. In other words, the creation of goods and services depends upon money changing hands. Zander's proposal is much more rational. It puts the horse properly before the cart, in that producers can create a form of money themselves with which to enable the purchase of their products. In this instance the creation of money depends upon goods or services changing hands.

When an economic entity, such as the Railway, must pay for what it needs in official currency, it must first acquire the currency to get what it needs. Alternatively it might purchase what it needs on credit in anticipation of having the cash it needs to pay at the time the bill comes due. However, in doing this, it commits itself to deliver something (money) which it only hopes to obtain. As Zander points out,

"Whether its hope will materialize is uncertain. The undertaking to pay at maturity contains, therefore a speculative element, which is particularly hazardous in times of depression. But the railway can promise to pay something else, namely, to transport commodities and persons; that is to fulfill its function as a railway. There is nothing speculative about that. The means required for this, rolling stock and other plant, are available. This is therefore fundamentally different from a promise to pay cash at a future date, for in the latter case the means of payment have yet to be secured, and this by having transported passengers and goods. The capacity of the railway to act as a carrier is, on the contrary, unquestionable."

The essential features of the Zander plan are:

The primary feature in maintaining their value is the commitment of the Railway to accept the certificates at any time at their face value, regardless of their market rate.

Since the Railway certificates are not legal tender, traders in the market are free to refuse them or to accept them at a discount from their face value. The value of the certificates depends upon the ability of the Railway to deliver that which the certificates promise -- railway services. If the Railway should somehow over-issue, the market would react by discounting the certificates, e.g. accepting them at 95% of face value. This would tend to increase the demand for them among users of railway services, since they could now obtain a dollar's worth of service for only 95 cents. This would furthermore induce the Railway to reduce the amount of certificates in circulation. If it did not do so it would suffer a loss in profitability. It is in this way that a free currency is self-correcting.

In the early 1970's, Dr. Ralph Borsodi, political economist, social philosopher and founder of the School of Living, [47] together with a few associates, developed and launched a currency experiment called the "Constant." Concerned about the chronic inflation resulting from official debasement of the dollar, Borsodi conceived a privately issued currency which would hold its value.

Borsodi's basic strategy for making his currency inflation-proof was to make it redeemable for a "market basket" assortment of basic commodities. The development of the Constant never progressed that far, but the Constants that were issued were backed by bank deposits of dollars. Constants circulated successfully for almost 2 years and enjoyed wide acceptance by the public. At its peak, the equivalent of about $160,000 in Constants was circulating throughout southern New Hampshire and elsewhere, both in the form of paper currency and as checking account balances at several area banks. News of the Constant was reported in several popular publications, such as Forbes and Business Week, in addition to numerous New England dailies.

Why Borsodi did not complete his plan for backing the Constant with commodities is not entirely clear. His advancing age and failing health may have been factors, along with possible organizational problems and lack of sufficient capital. [48] Figures 8.7 and 8.8 show the front and reverse sides, respectively, of a 25 Constant note.

|

|

As early as 1914, Bilgram and Levy proposed a "credit clearance" system. [49] They introduced their plan with the following statement:

"Were a number of businessmen to combine for the purpose of organizing a system of exchange, effective among themselves, they could clearly demonstrate how simple the money system can really be made. The greater the number of businessmen that would thus cooperate, the more complete would be their own emancipation from the obstruction to commerce and industry which existing currency laws impose."

The plan which Bilgram and Levy outlined was basically as follows:

Most all businesses have accounts payable and accounts receivable. This plan provides a means of clearing the major part of these balances.

Mutual Credit and LETS systems are conceptually similar to Bilgram and Levy's Credit Clearance plan. Their plan, however, required that members deposit "security" in the form that conventional banks require, i.e. bonds, stocks, mortgages, etc.. Mutual Credit and LETS consider this to be an unnecessary burden, and require only the member's commitment to accept credits in payment. The rationale is that the privilege of continuing participation in the system will be sufficient inducement for members to honor their commitments. In the case of Mutual Credit systems, debit balances are limited to some amount determined by a member's trading volume, while LETS, as originally conceived, imposes no debit limits.

Further, neither Mutual Credit or LETS require debtors to deposit official money or allow creditors to withdraw official money, except that Mutual Credit, as conceived, requires a member upon withdrawing from the system, to clear any remaining debit balance with cash if s/he cannot deliver sufficient credits.